While the process may seem convoluted, having the right plan to repay federal student loans is vital to managing your debt. For more details on the repayment options from MyFedLoan, please review our complete guide.

Learning more about Federal Student Loan Repayment Plans

Federal student loans come with several repayment plans with varying financial demands. These plans fall into two categories: fixed repayment plans and income-driven repayment (IDR) plans.

Fixed Repayment Plans

- Standard Repayment Plan

- Terms: 10 years, with a fixed monthly payment.

- Who It’s Best For: Borrowers who want to pay off loans quickly with regular payments.

- Pros: Less total interest paid throughout your loan.

- Cons: Monthly payments are higher than no-deductible plans.

- Graduated Repayment Plan

- Payments start low, then adjust up every couple of years over a 10-year term.

- Best For: Borrowers who anticipate their income will grow slowly over time.

- Pros: Smaller initial payments allow for a smoother transition into repayment.

- Cons: You pay more total interest because the initial payments are lower.

- Extended Repayment Plan

- Terms: Fixed or graduated payments spanning up to 25 years.

- Best For: Big borrowers wanting slim monthly payments.

- Pros: Lower dollar amounts for monthly payments.

- Cons: Much more interest is paid over the life of the loan.

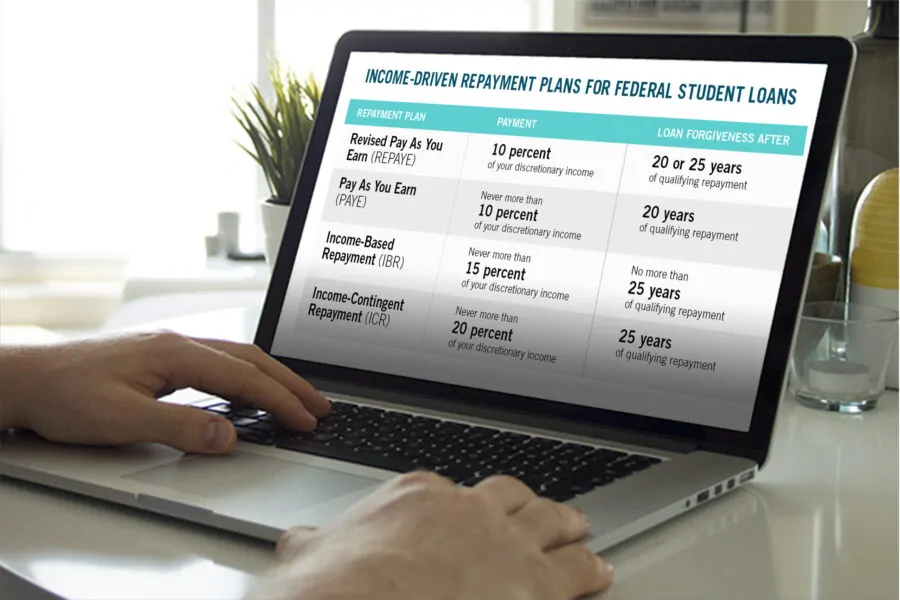

Plans of Income-Driven Repayment (IDR)

IDR—Monthly payment plans tailored to suit income and family size and allow for flexibility in the time frame for repayment; this might be the best way out for students (and new graduates) from that tough spot.

- SAVE (Saving on a Valuable Education) Plan

- Structure: Payments based on a percentage of discretionary income; forgiven after 20 or 25 years.

- Best Risks: Low debt-to-income borrowers.

- Pros: Smaller monthly payments; possible forgiveness of remaining balance.

- Pros: No income verification needed annually; lower overall interest paid potential.

- As You Pay As You Earn (PAYE)

- Structure: Limited to 10% of discretionary income. Forgiveness after 20 years.

- Ideal for: New graduates with a high ratio of debt to income.

- Pros: Reduced payments; interest subsidy advantages.

- Pros: Stringent eligibility criteria; needs to be recertified annually.

- Based on Income Repayments (IBR)

- How it works: You pay 10-15% of your extra income each month, and after 20 or 25 years, the debt is canceled.

- Best For: Those with debt-to-income or high-debt balance measures and a portion of financial hardship.

- Pros: Easier qualification; potential for forgiveness.

- Pros: Payments are higher than those under PAYE for some; annual recertification is needed.

- Income-Contingent Repayment (ICR)

- Structure: Payment as much as 20 percent of discretionary income or fixed over 12 years at her discretion; forgiveness in 25 years.

- Best For: Borrowers of a Parent PLUS loan who consolidate into a Direct Loan.

- Pros: Open to all borrowers; can vary payment amounts.

- Cons: Higher payments are possible, but there is a longer repayment time.

Selecting an Appropriate Repayment Plan

Determining which repayment plan is right for you requires some evaluation of your financial situation, career path, and eventual ambitions. Think about these factors:

- Current Income and Expenses: Assess the ability to make monthly payments.

- Prospects to Earn: You may exclude future changes in earnings relevant to the change of repayment ability.

- Loan Balance: Higher balances might benefit from extended or income-driven plans.

- Follow a Forgiveness Goal: Some payment plans will forgive your debt after some years, which can be helpful.

Using Loan Simulator and other tools can help you better understand how different plans relate to your unique financial circumstances.

Changing Your Repayment Plan in 5 Easy Steps

- Contact Your Loan Servicer: Connect to MyFedLoan through a click or a call to find out your options and get started.

- Fill Out Required Forms: If a repayment plan is available, you will need to fill out and submit the documentation or application.

- Submit Income Documentation: IDR plans require verification of your income and household size.

- Recertify Each Year: On IDR plans, you must resubmit your income and family size every year to remain eligible.

FAQ’s

Whose services cover my federal student loans?

To get your servicer’s contact information, go into your StudentAid.gov account and scroll to the “My Loan Servicers” area.

Can federal student loan forgiveness be offered for public service in repayment plans?

Under a qualifying repayment schedule, the Public Service Loan Forgiveness (PSLF) program forgives outstanding loan amounts after 120 qualifying payments as a full-time employee for a qualified company.